US stock markets showed solid gains on Thursday, with gold prices reaching a new all-time high. Investors are optimistic about the upcoming Federal Reserve meeting, expecting an interest rate cut as early as next week.

The key US indices fluctuated in mixed territory for most of the trading day, but showed solid gains by the close. The European Central Bank's recent decision to cut interest rates and slightly better-than-expected U.S. producer price data helped fuel the rally. Despite this, investors remain confident that the Fed will cut rates slightly at its next meeting.

The Dow Jones Industrial Average added 0.58%, the S&P 500 rose 0.75%, and the tech-heavy Nasdaq Composite rose 1%. Strong results from tech companies helped the Nasdaq take the lead in growth.

The MSCI World Equity Index, which measures markets around the world, rose 1.08%, confirming positive investor sentiment in global markets.

Earlier on Thursday, the European Central Bank announced its second interest rate cut in three months, which was driven by slowing inflation and weakening economic growth in the eurozone. The cut was predictable, but the ECB has yet to give clear signals about its future plans.

While the 0.25% rate cut did not come as a surprise to the market, the question remains as to how decisively and quickly the central bank will act in the remaining months of the year.

Market participants are now focused on the upcoming Federal Reserve meeting, which will decide on the key interest rate on Wednesday. Investors are expecting the Fed to make the first rate cut since 2020. However, fresh economic data released on Thursday suggest that the Fed will likely limit the rate cut to 25 basis points, rather than the larger 50 basis point cut that some analysts had previously expected.

An important factor for the upcoming Fed decision was the inflation data released on Wednesday and Thursday. The indicators point to a slight increase in prices, but the rate of inflation remains relatively low. Thus, the core consumer price index increased by 0.28% in August, which is higher than the expected growth of 0.2%. In addition, the data on producer prices also exceeded expectations: in August, they grew by 0.2% instead of the expected 0.1%. Despite this, the general trend remains in favor of slowing inflation, which increases the likelihood of a moderate rate cut.

Amid expectations of a rate cut, the US dollar showed weakness against major world currencies. The dollar index, which tracks its dynamics against a basket of leading currencies, fell by 0.52%, reaching 101.25. At the same time, the euro strengthened by 0.54%, reaching $1.1071. This trend reflects global changes in investor sentiment, who expect further easing of monetary policy in the United States.

Oil prices continued their upward movement, adding almost 3%, amid investor concerns about how severely U.S. crude output will be affected by Hurricane Francine in the Gulf of Mexico. On Thursday, producers announced forced production cuts, but there were signs that some export ports were partially reopening.

WTI crude rose 2.72% to $69.14 per barrel, while benchmark Brent crude rose 2.21% to $72.17 per barrel.

Gold prices soared to all-time highs as expectations of an imminent Fed rate cut made the precious metal even more attractive for investment. Amid market instability, gold has once again confirmed its status as a "safe haven" for capital.

Spot gold rose 1.85% to a record $2,558 an ounce, while U.S. gold futures rose 1.79% to settle at $2,557 an ounce.

U.S. Treasury yields also showed modest gains. The two-year yield rose 1.2 basis points to 3.6579%. The 10-year yield rose 3 basis points to 3.683%.

The Producer Price Index (PPI), which tracks changes in the cost of goods and services at the producer level, rose 0.2% in August, beating expectations for a 0.1% gain. The core measure, which excludes volatile items such as food and energy, rose 0.3%, also beating expectations for a 0.2% gain.

The number of initial jobless claims in the United States for the week ending September 7 was 230,000, which was in line with analysts' expectations. This data confirms the stable state of the American labor market, despite some macroeconomic fluctuations.

The latest economic reports show weakening employment and slowing economic growth, which has raised expectations for a deeper 50 basis point rate cut by the Federal Reserve. However, the release of inflation data on Wednesday changed the market sentiment, with traders now assessing the likelihood of a more modest cut.

Despite Thursday's fluctuations, CME's FedWatch tool showed that traders still have a 69% chance of expecting the Fed to cut interest rates by 25 basis points at the September 17-18 meeting. If that happens, it would be the first rate cut since March 2020, marking an important step in monetary policy.

Against these expectations, the Russell 2000 index of small-cap companies was the best performer among the indices, gaining 1.2%. That underscores confidence that small businesses can benefit from the upcoming easing of credit conditions.

All 11 industry sectors in the S&P 500 ended the day in positive territory. Communications services led the way, rising 2%. Warner Bros Discovery was particularly strong, jumping 10.4% after the company announced an agreement with Charter Communications to give customers access to ad-supported versions of its Warner Max and Discovery+ streaming services. Charter also posted a strong gain, gaining 3.6%.

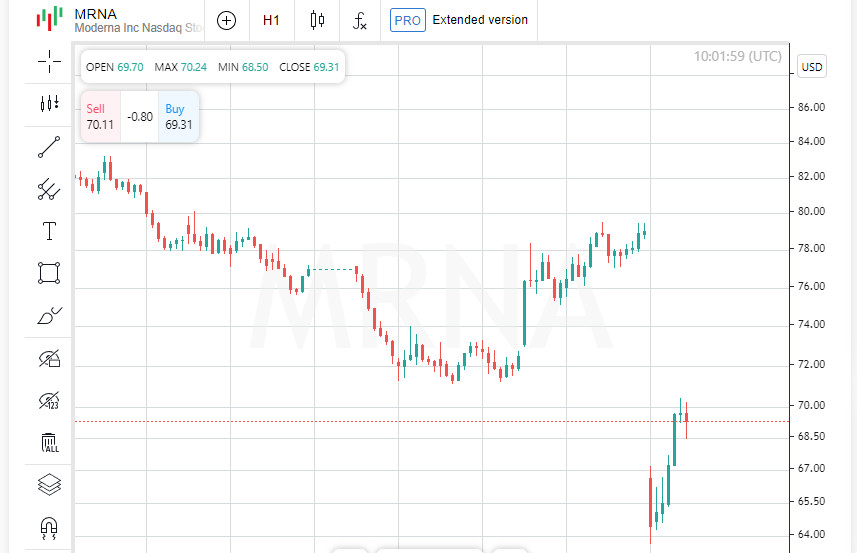

Not all stocks ended the day in positive territory. Shares of vaccine maker Moderna fell 12.4%, hitting their lowest since November last year. The company announced revenue guidance for next year in the range of $2.5 billion to $3.5 billion, which was lower than analysts expected, which caused the stock to fall.

One of the brightest news of the day was the rapid growth of shares of the supermarket chain Kroger, which rose by 7.2%. This happened because the company exceeded expectations for the second quarter results and raised the lower limit of its annual sales forecast. The optimistic report became a signal to investors that the chain is confidently coping with market challenges.

Shares of companies involved in gold mining sharply went up, following the rise in prices of the precious metal. The spot price of gold reached an all-time high, which led to a 5.8% increase in the Arca Gold BUGS index. Investors continue to view gold as a safe haven against market risk and inflation, fueling interest in the gold mining sector.

On the New York Stock Exchange (NYSE), advancers outnumbered losers by a wide margin, 3.45 to 1. There were 405 new highs and just 46 new lows, a strong showing for bulls.

On the Nasdaq, advancers also outnumbered losers by a wide margin, 1.73 to 1. The S&P 500 posted 37 new yearly highs and no new lows, signaling positive sentiment in the market, while the Nasdaq Composite posted 73 new highs and 76 new lows, showing more diversity in stock performance.

The total volume of shares traded on U.S. exchanges was 10.58 billion, just slightly below the 10.82 billion average over the past 20 trading sessions. This figure shows that activity in the markets remains strong despite some swings in individual sectors.

QUICK LINKS

Contact Us

Contact Us