Yesterday, stock indices showed mixed results. The S&P 500 rose by 0.24%, while the Nasdaq 100 fell by 0.63%. The Dow Jones Industrial Average declined by 0.22%.

The dollar strengthened slightly, and Treasury bonds reversed some of their recent gains after US labor market data did little to bolster arguments for further cuts in the Federal Reserve's interest rates. Oil prices increased following President Donald Trump's escalation of pressure on Venezuela.

The American currency appreciated against all major G10 currencies, especially the yen. The yield on Treasury bonds decreased across the curve, rising by more than two basis points to 4.17%. Notable fluctuations were observed in the commodities market: oil prices surged by 1.3% after Trump ordered a blockade on tankers heading to and from Venezuela, raising concerns about supply from this OPEC member. Silver soared to a record high of $66 per ounce, while gold approached its historical peak. Platinum reached its highest level since 2008.

Tech stocks also rebounded after a two-day sell-off, with shares of the Chinese chipmaker MetaX Integrated Circuits Shanghai Co. soaring by an astonishing 755% in their debut trading session. The latest US labor market data point to a cooling labor market but not a rapid weakening, prompting traders to refrain from predictions regarding further interest rate cuts by the Fed in the near future. After the report was released on Tuesday, markets assigned a roughly 20% probability to a rate cut in January.

Attention now turns to inflation data set to be released on Thursday, which could indicate whether the economic landscape might change during the last full trading week of the year. Analysts at Evercore ISI stated that they view the employment report with optimism and believe that the Federal Reserve shares this perspective. According to them, the report was not weak enough to warrant another interest rate cut in the near future.

As a reminder, in November, non-farm payrolls increased by 64,000 after a decrease of 105,000 in October. The unemployment rate was 4.6%, up from 4.4% in September.

As noted earlier, the price of gold is nearing its record high of $4,381 set in October. The precious metal has appreciated by about two-thirds this year, heading for its best annual performance since 1979, driven by active purchases from central banks and a general outflow of investors from bonds.

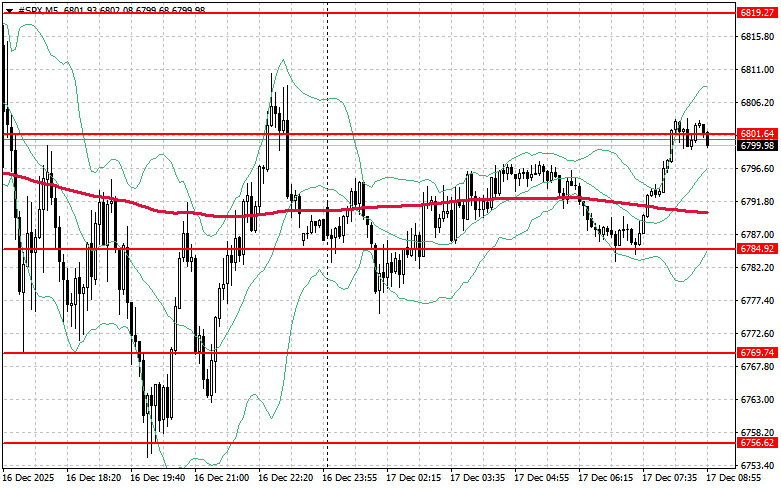

Regarding the technical outlook for the S&P 500, today's primary task for buyers will be to overcome the nearest resistance level of $6,801. Successfully doing so could signal growth and pave the way for a surge to a new level of $6,819. An equally critical task for bulls will be to secure control above $6,821, which would strengthen their positions. In the event of a downward movement amid declining risk appetite, buyers must make a stand around $6,784. A break below this level could quickly push the trading instrument back to $6,769 and open the path down to $6,756.

QUICK LINKS

Contact Us

Contact Us